Interest Calculation and Posting

The total amount to be repaid for a loan includes both the principal and the interest charged over the loan period.

The interest rates charged on loans are determined according to the SACCO Policy, which is regulated by SASRA.

Each loan product has a minimum interest rate set up in the system — the rate charged to a specific client can vary, but it must remain within the policy limits.

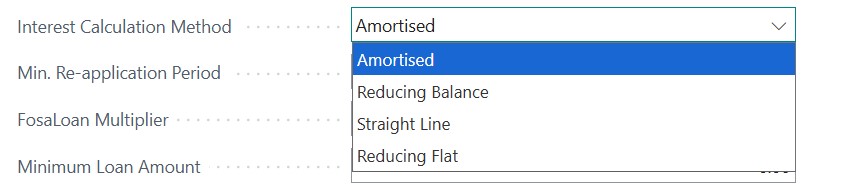

Interest Calculation Methods

There are four main types of interest calculation methods commonly used across loan products:

1. Amortised Method

For this method, the loan is repaid through equal periodic installments, which include both principal and interest.

Over time, the interest portion of the repayment decreases because it is calculated based on the remaining principal after each repayment, while the total payment remains the same.

Commonly used in: Mortgages, car loans, and long-term personal loans.

2. Reducing Balance Method

In this method, interest is calculated on the remaining principal, not on the original amount borrowed.

As the principal reduces with each repayment, the interest amount decreases over time.

This results in a lower total interest compared to flat-rate methods.

3. Reducing Flat Method

With this method, interest is calculated on the original principal, but the repayment schedule is structured in a way that reduces the principal over time.

This sometimes results in slightly lower total interest than a traditional flat-rate calculation.

Acts as a middle ground between flat and reducing balance methods.

4. Straight Line Method

For this method, interest is calculated on the original principal for the entire loan period.

The interest amount remains constant throughout the loan term.

This method is simple but usually results in the highest total interest paid over time.

Loan Product Setup

The interest calculation method is defined during loan product setup based on the SACCO policy.

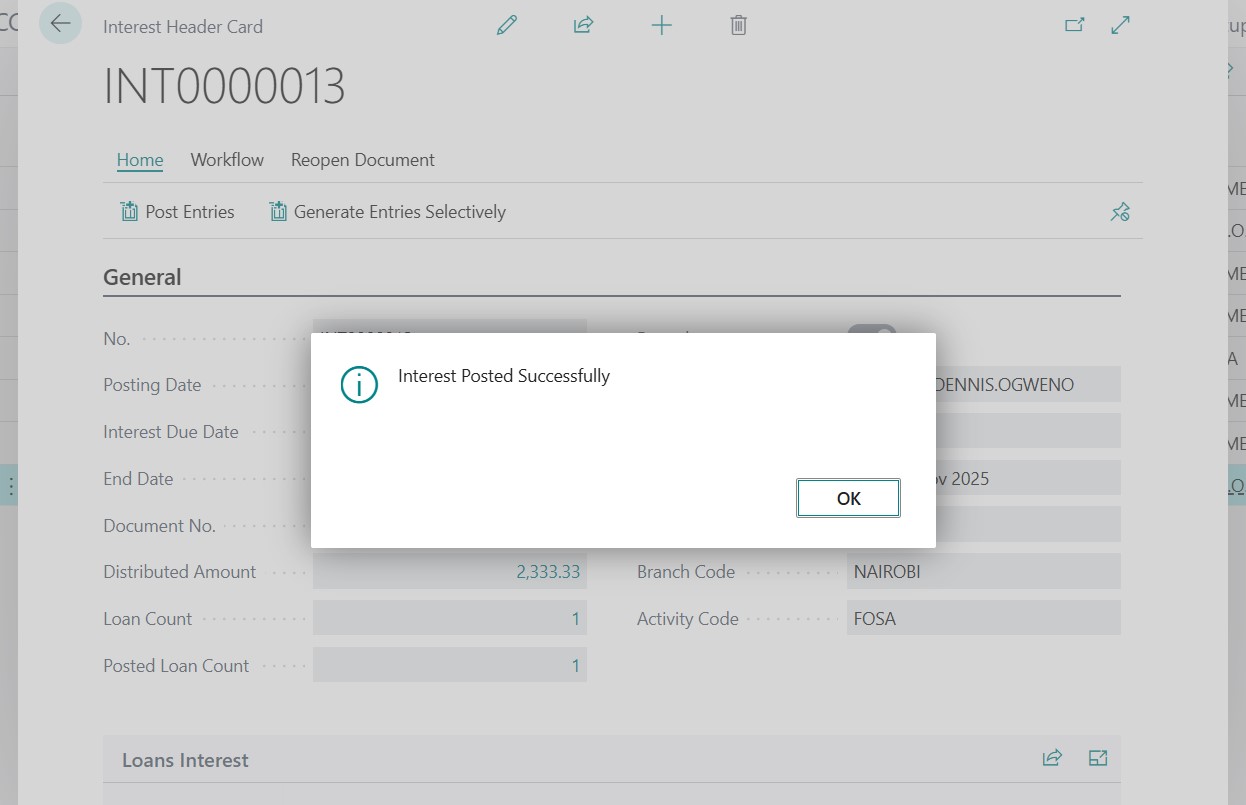

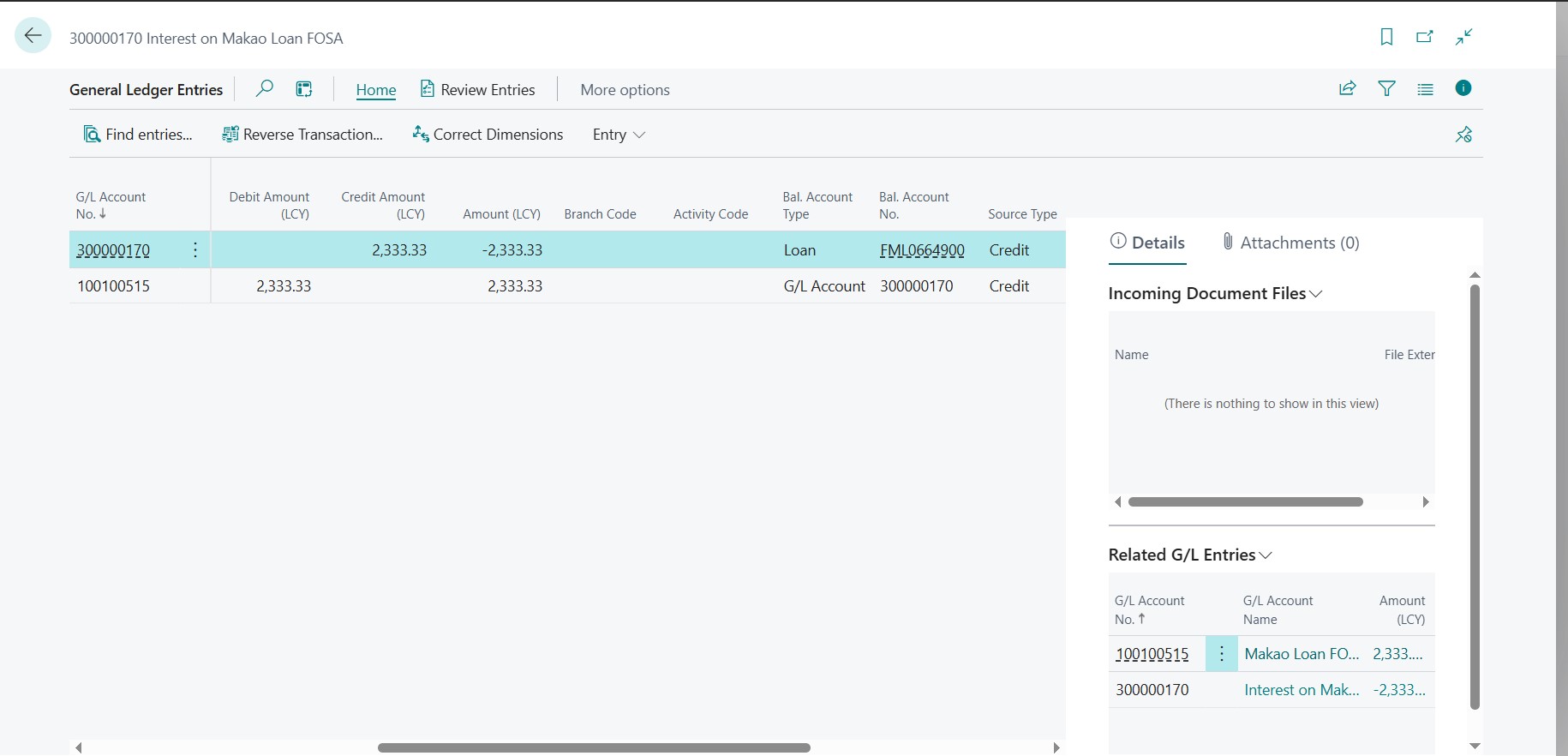

Once the interest is charged, it is posted — updating the relevant General Ledger (G/L) and Loan Accounts:

- Credit: Loan Account

- Debit: Interest Income G/L Account

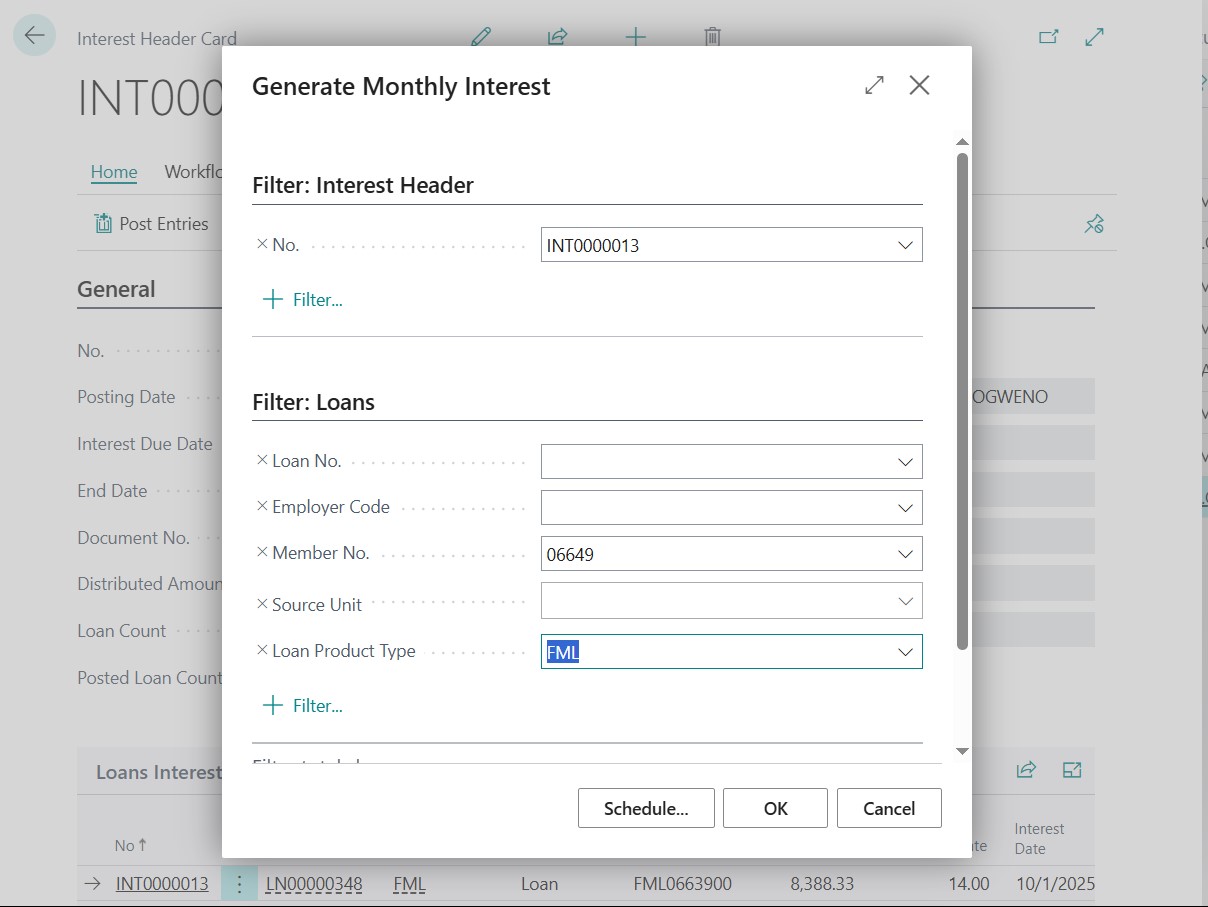

Interest Calculation Process

For the loan at hand, interest is first calculated for a specific billing period.

Interest can be calculated specifically for individual loans or generally for all applicable loans, using filters in the system.

Once interest is generated, it is posted to the relevant Credit and G/L Accounts, and the loan repayment is determined as the sum of:

- The Interest Amount, and

- The Principal Repayment for the loan.

Summary

| Method | Interest Basis | Payment Structure | Interest Trend | Typical Use |

|---|---|---|---|---|

| Amortised | Remaining Principal | Equal Installments | Decreases | Mortgages, long-term loans |

| Reducing Balance | Remaining Principal | Decreasing Interest | Decreases | Personal & SACCO loans |

| Reducing Flat | Original Principal (Adjusted) | Semi-decreasing | Slightly Decreases | Retail loans |

| Straight Line | Original Principal | Constant | Fixed | Short-term or simple loans |

The method chosen during loan setup directly affects how repayments are structured, how interest accrues, and how postings are reflected in the SACCO’s financial records.