Sacco Loan Appraisal and Approval

Audience: Loan Officers, Credit/Appraisal Analysts, Branch Managers/Approvers, System Admins Version: 2025-11-05

Overview

This guide is a complete user reference for Sacco loan Appraisal and Approval processes in Business Central.

Process Flow

- Initiated Application Intake

- Appraisal (data capture, eligibility)

- Generate Payment Schedule

- Appraisal Report

- Send for Approval

- Approver Decision

- Ready for Disbursement

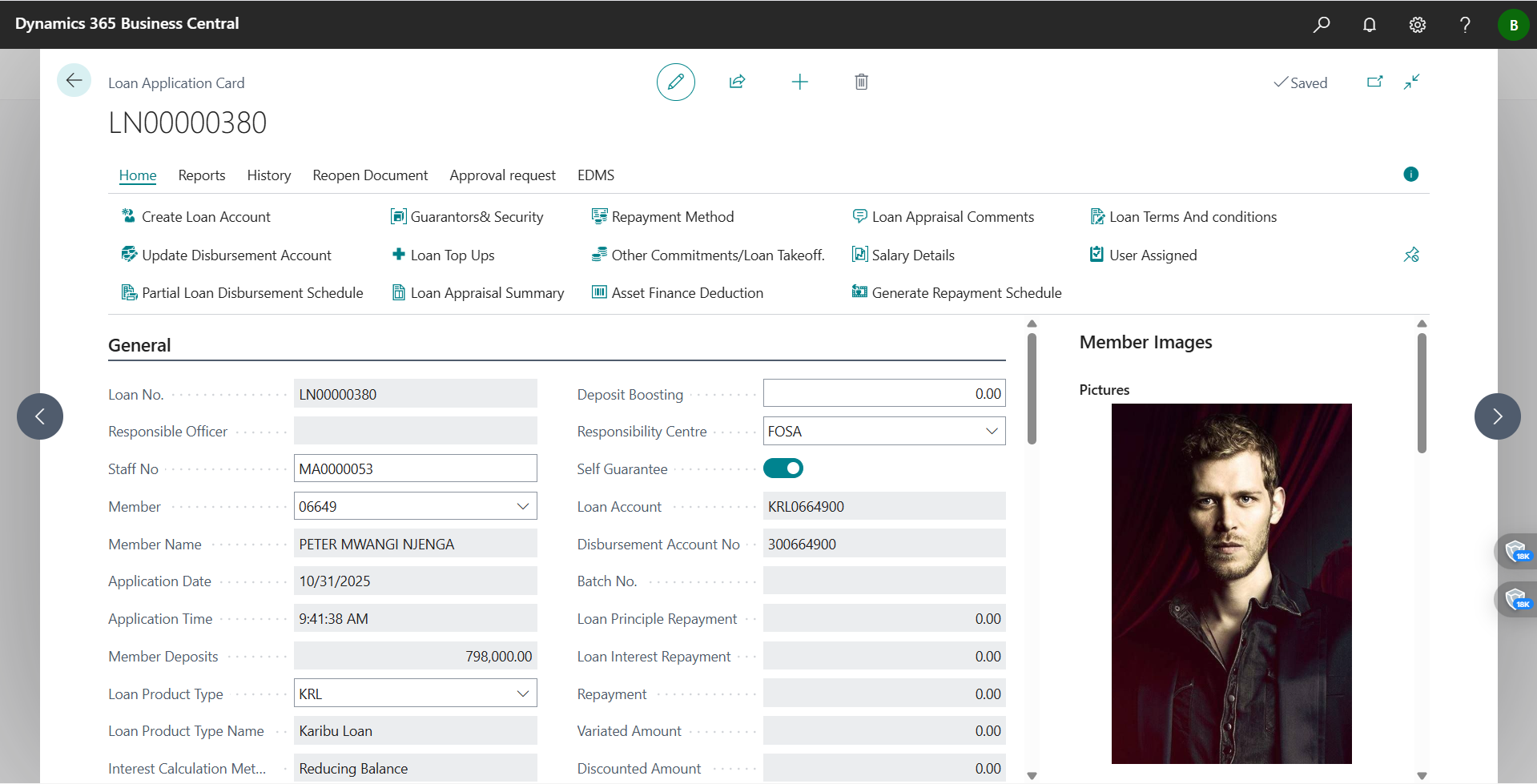

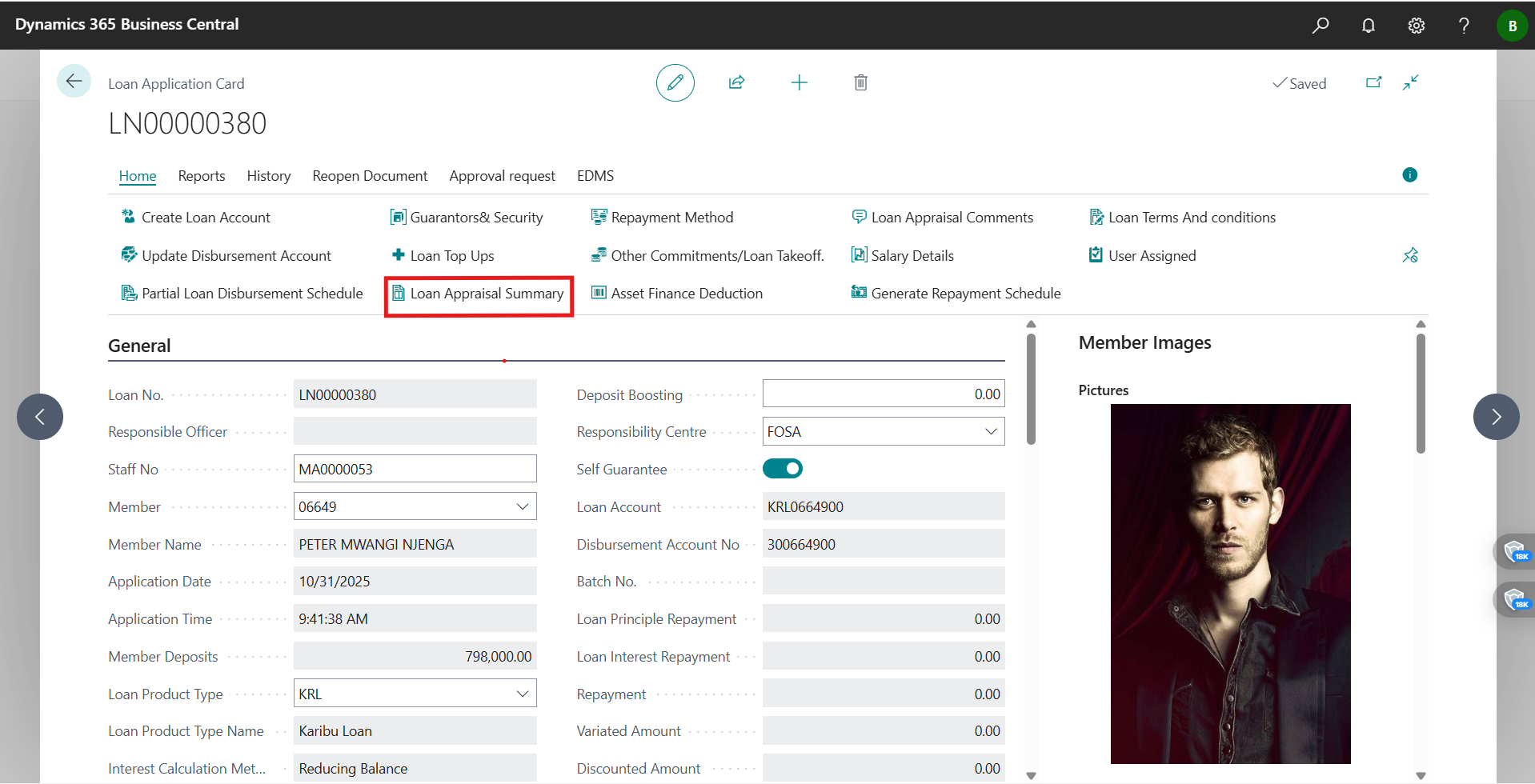

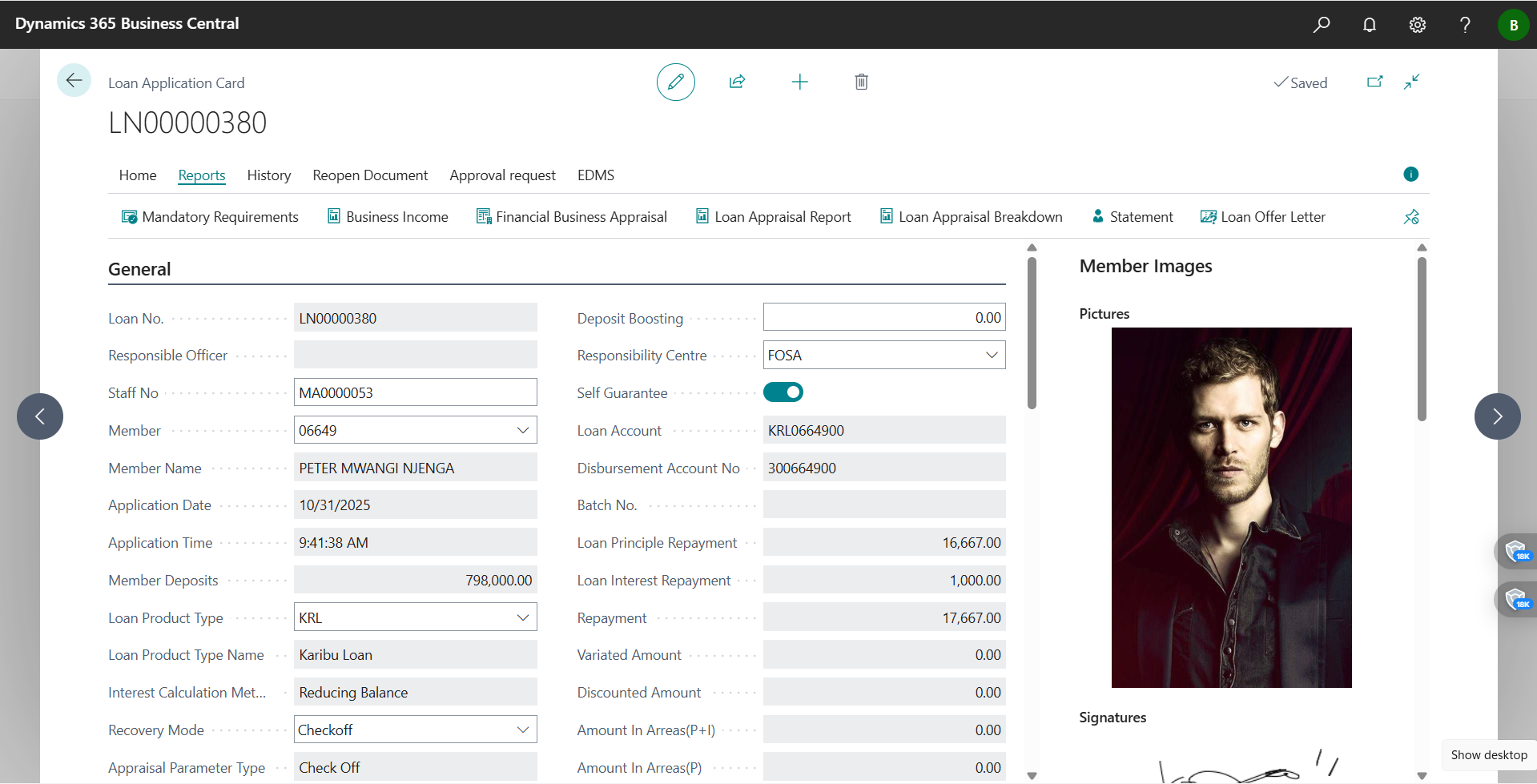

Step 1 — Start the Appraisal from the Loan Application

- On the Loan Application card, click the Appraisal action to expose the appraisal tools.

- Outcome: I can now access Eligibility Breakdown, Generate Payment Schedule, and Generate Appraisal Report.

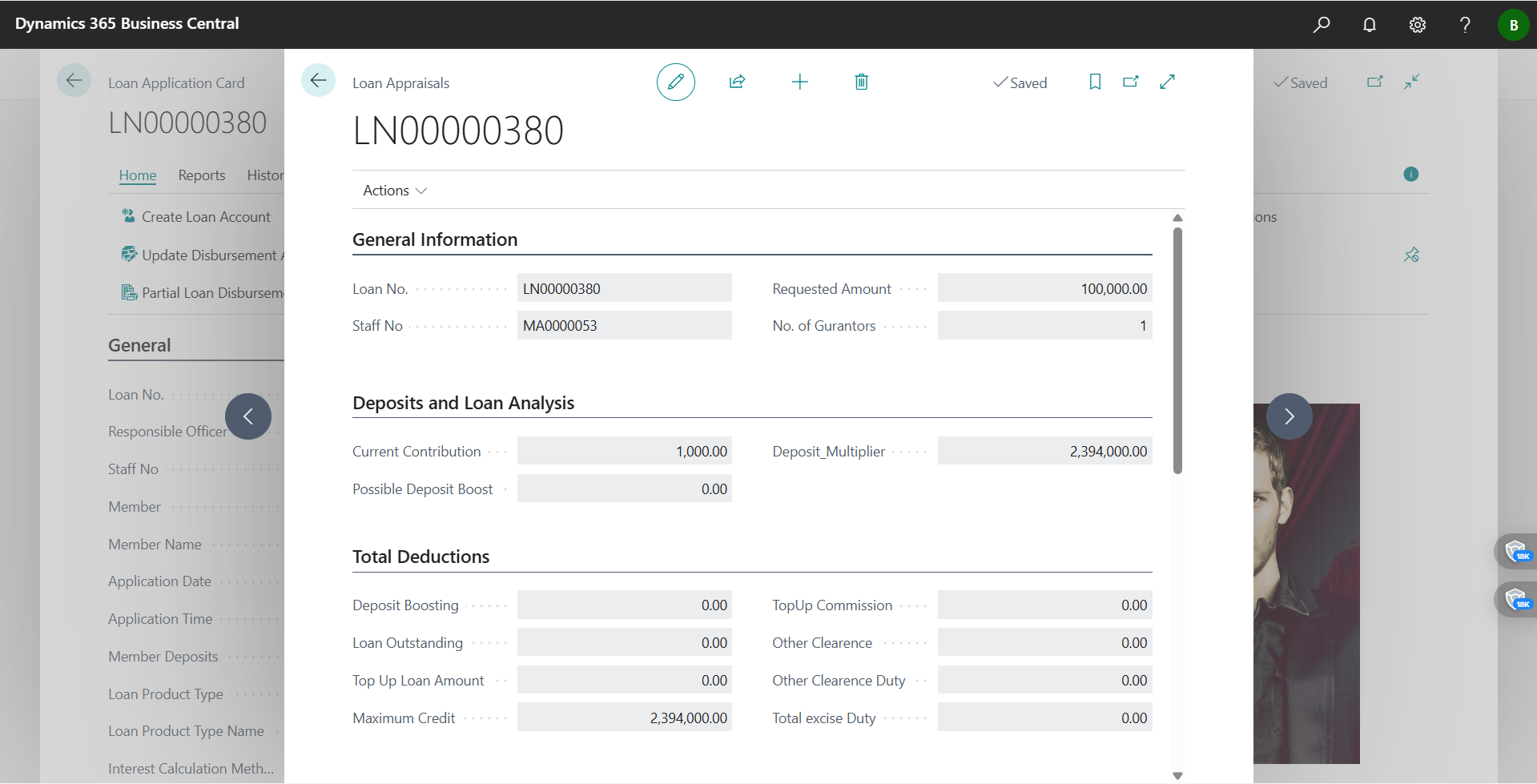

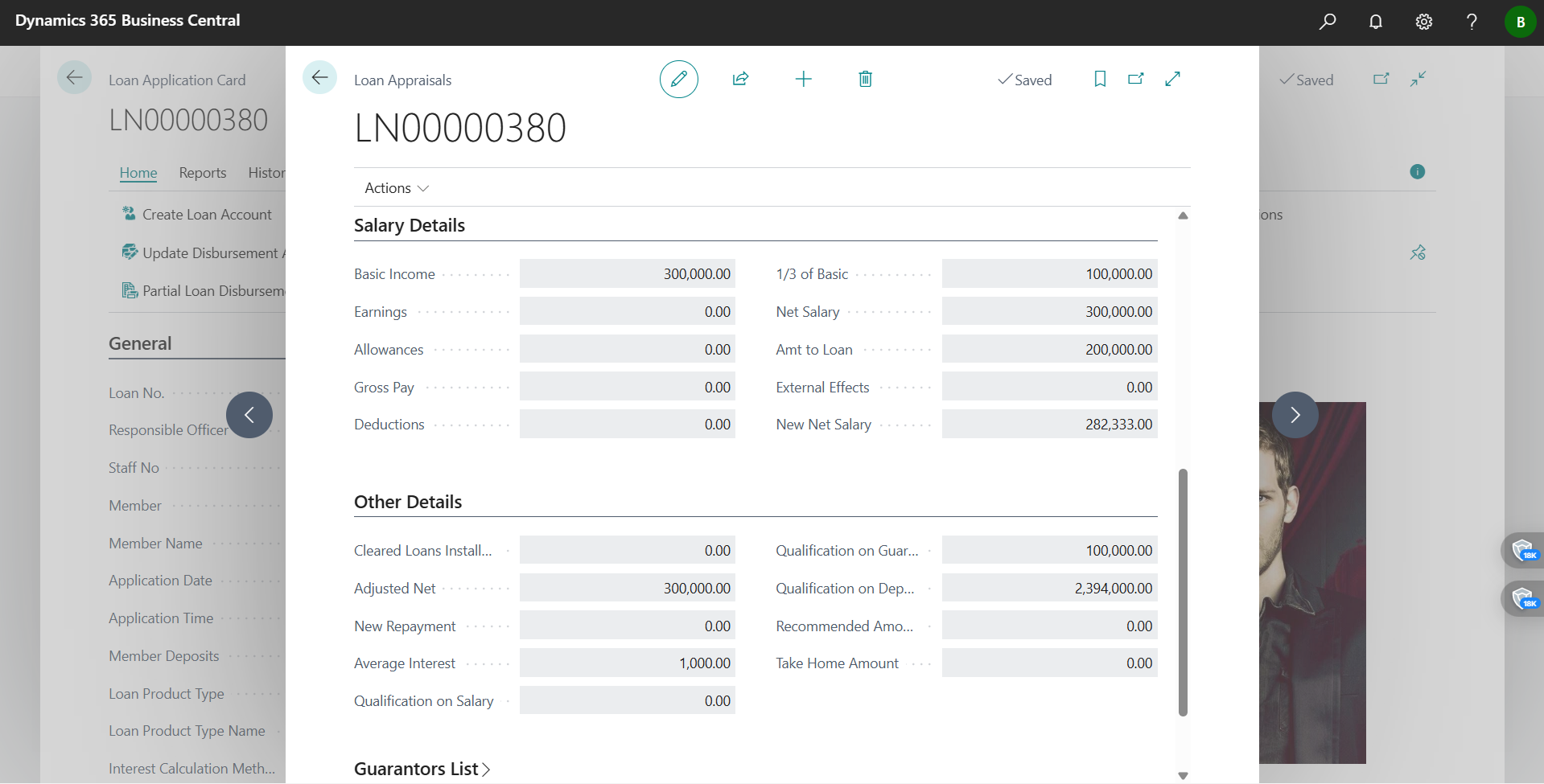

Step 2 — Capture the appraisal details (financials, collateral, guarantors)

- Enter member income, other recurring income, existing loan obligations, deductions/expenses, and then capture collateral and guarantors as needed.

- check on the standard appraisal form to double‑check inputs and attach it to the application.

- Visuals for the card/views I worked on:

- Appraisal form: Loan Appraisal form.pdf

- Appraisal form: Loan Appraisal form.pdf

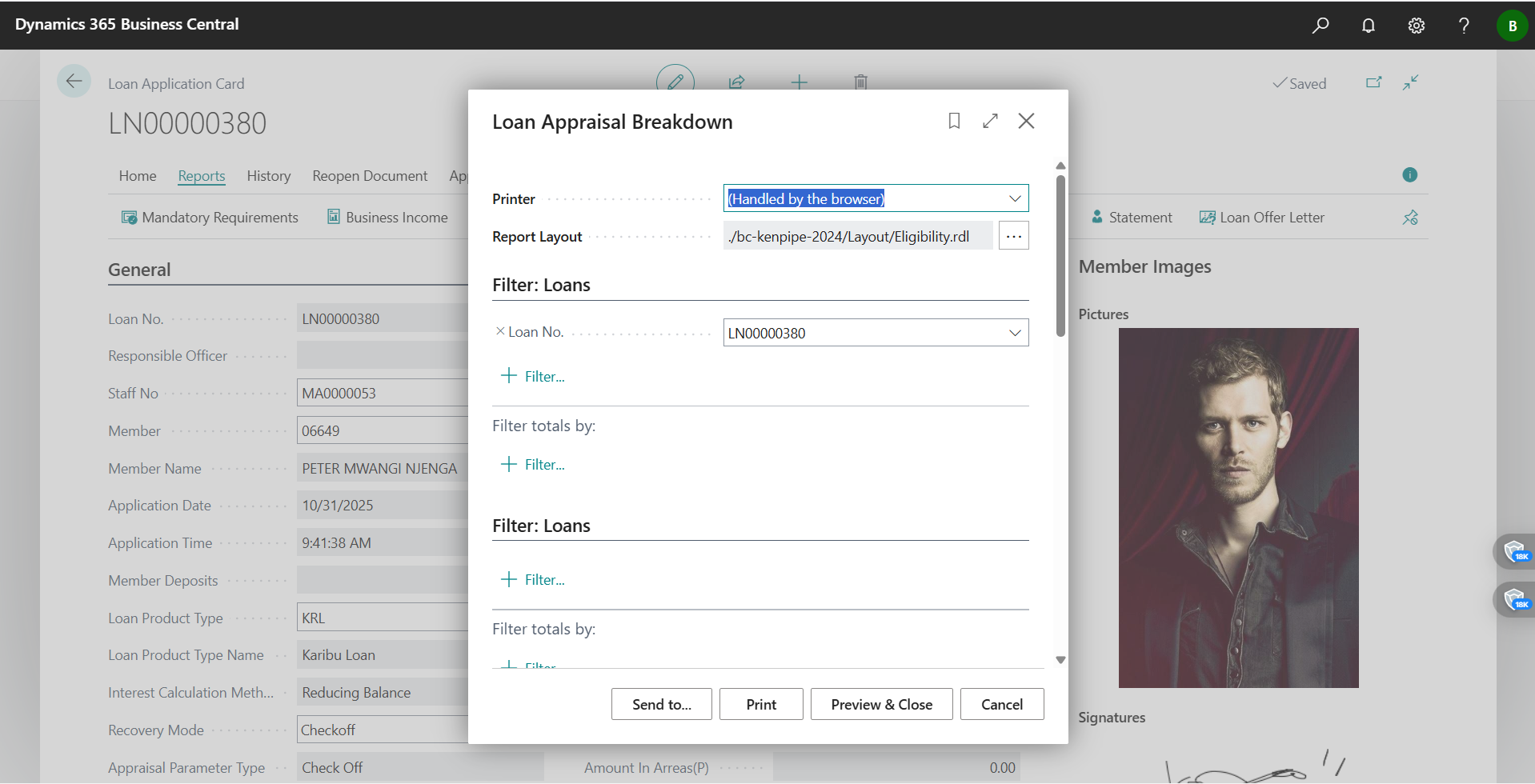

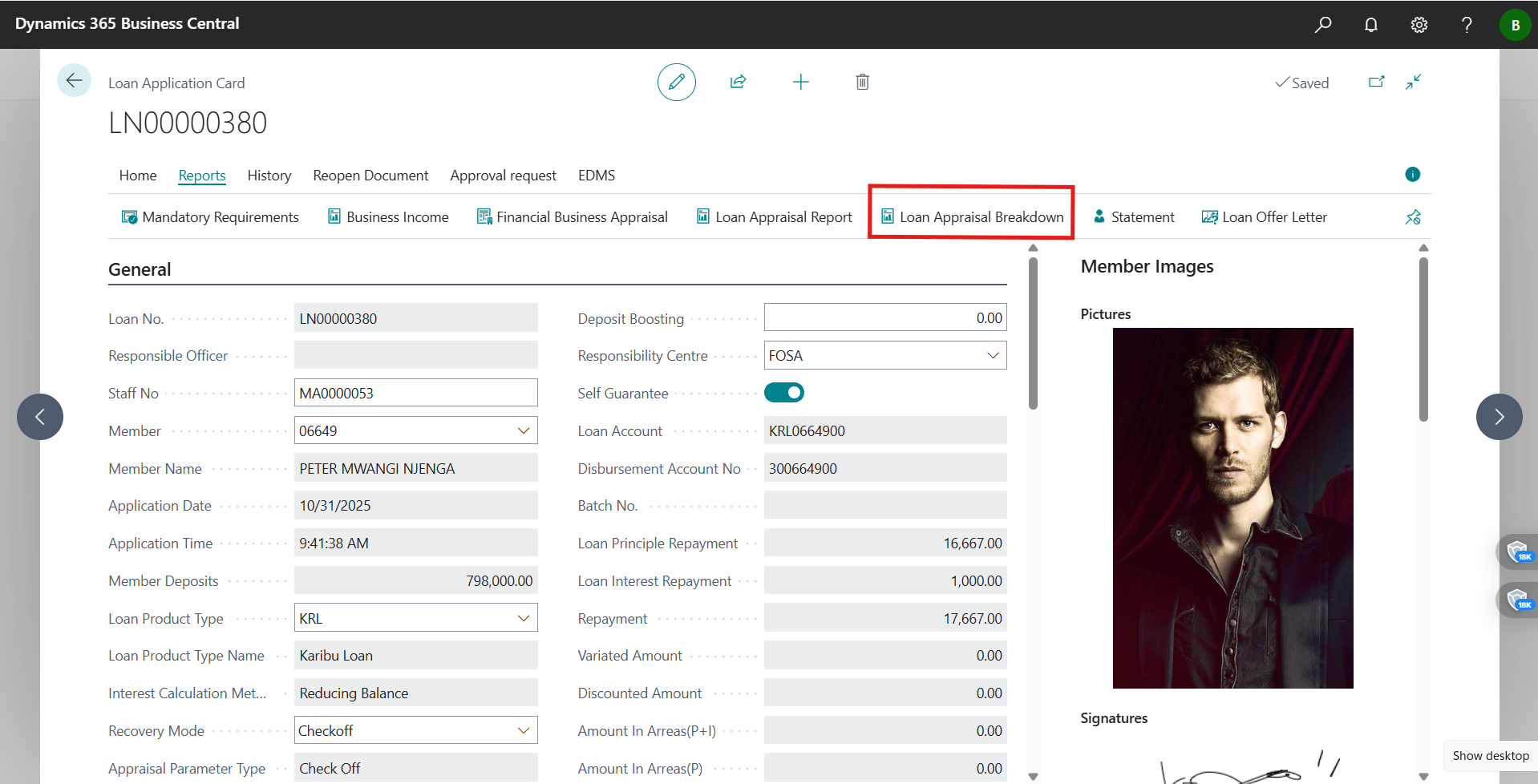

Step 3 — Run the Eligibility Breakdown and read the KPIs

- Choose Appraisal > Eligibility Breakdown to calculate eligibility based on the captured financials and product rules.

- Compare what you see on screen to the PDF to validate figures (share multiple cap, DTI, recommended amount/term, and any exception flags).

- Visuals:

- On-screen breakdown:

- Detailed reference: loan eligibility breakdown.pdf

- On-screen breakdown:

- What to check before moving on:

- Requested vs. share‑multiple cap

- DTI against product threshold (note any exception)

- Recommended amount/term and conditions I must enforce

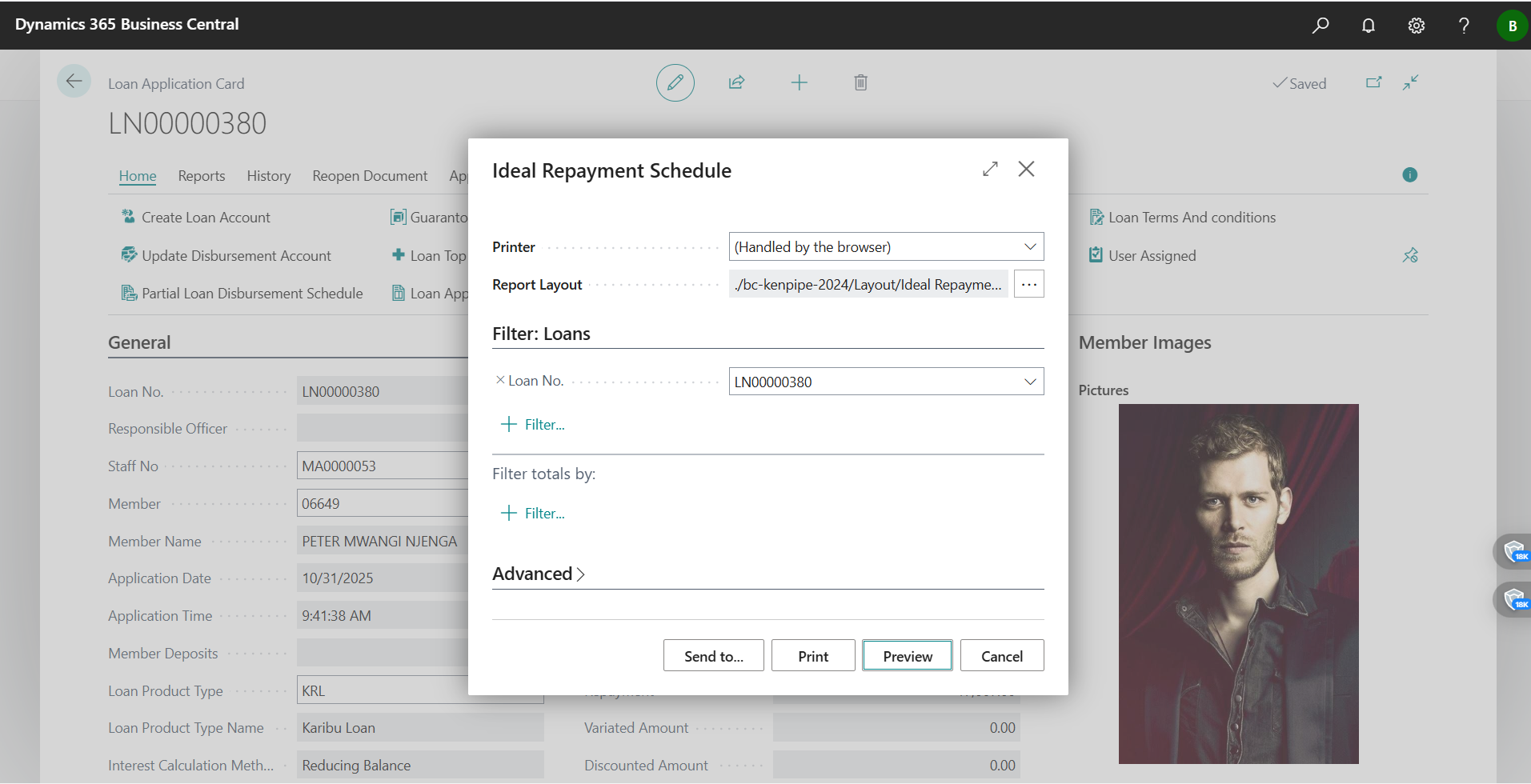

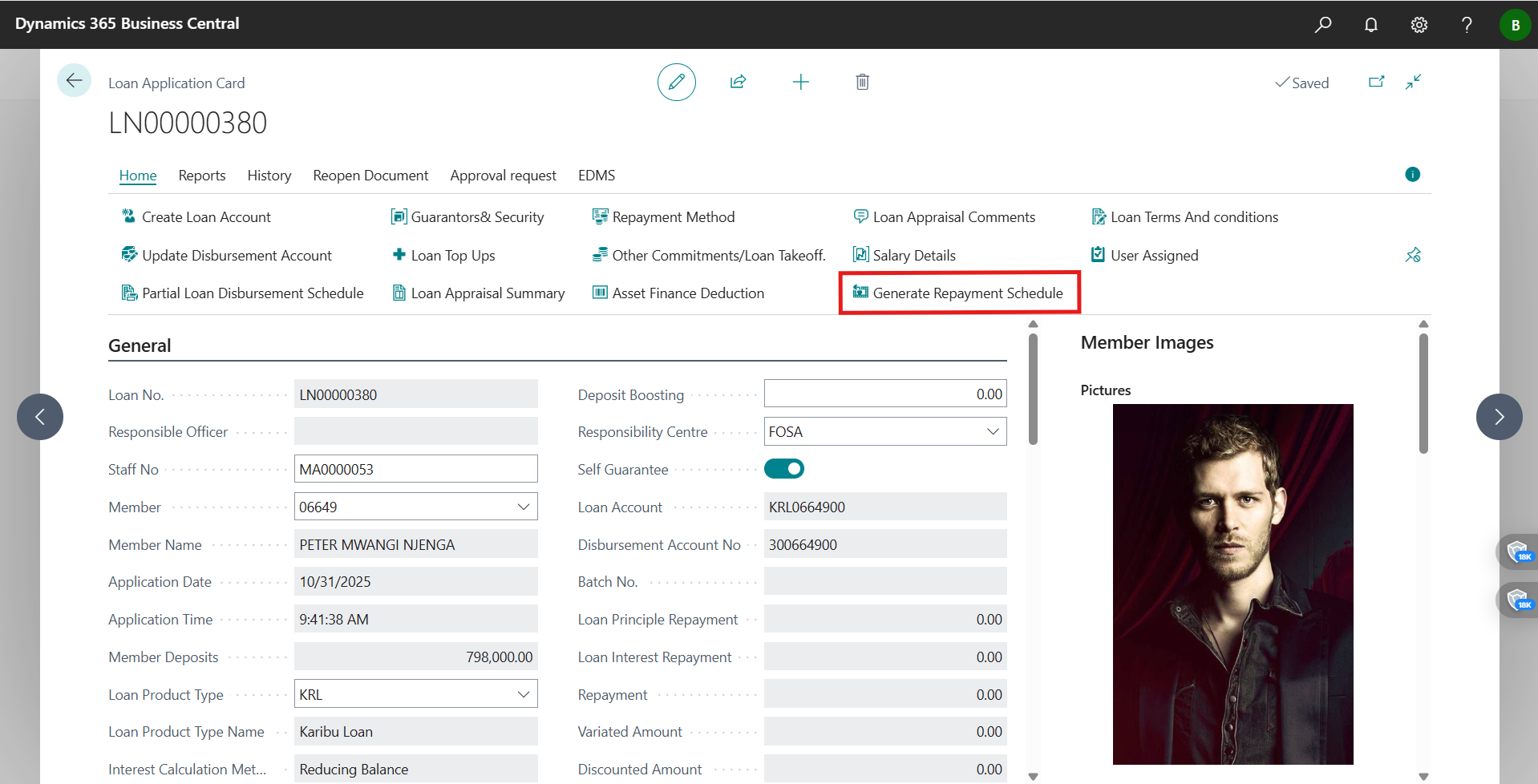

Step 4 — Generate a Payment Schedule to validate affordability

- Click Appraisal > Generate Payment Schedule and confirm Principal, Rate, Term, Frequency, Grace (if any), and First Installment Date.

- Make sure installments, dates, and totals look right for the method (reducing/flat) before I commit.

- Visual:

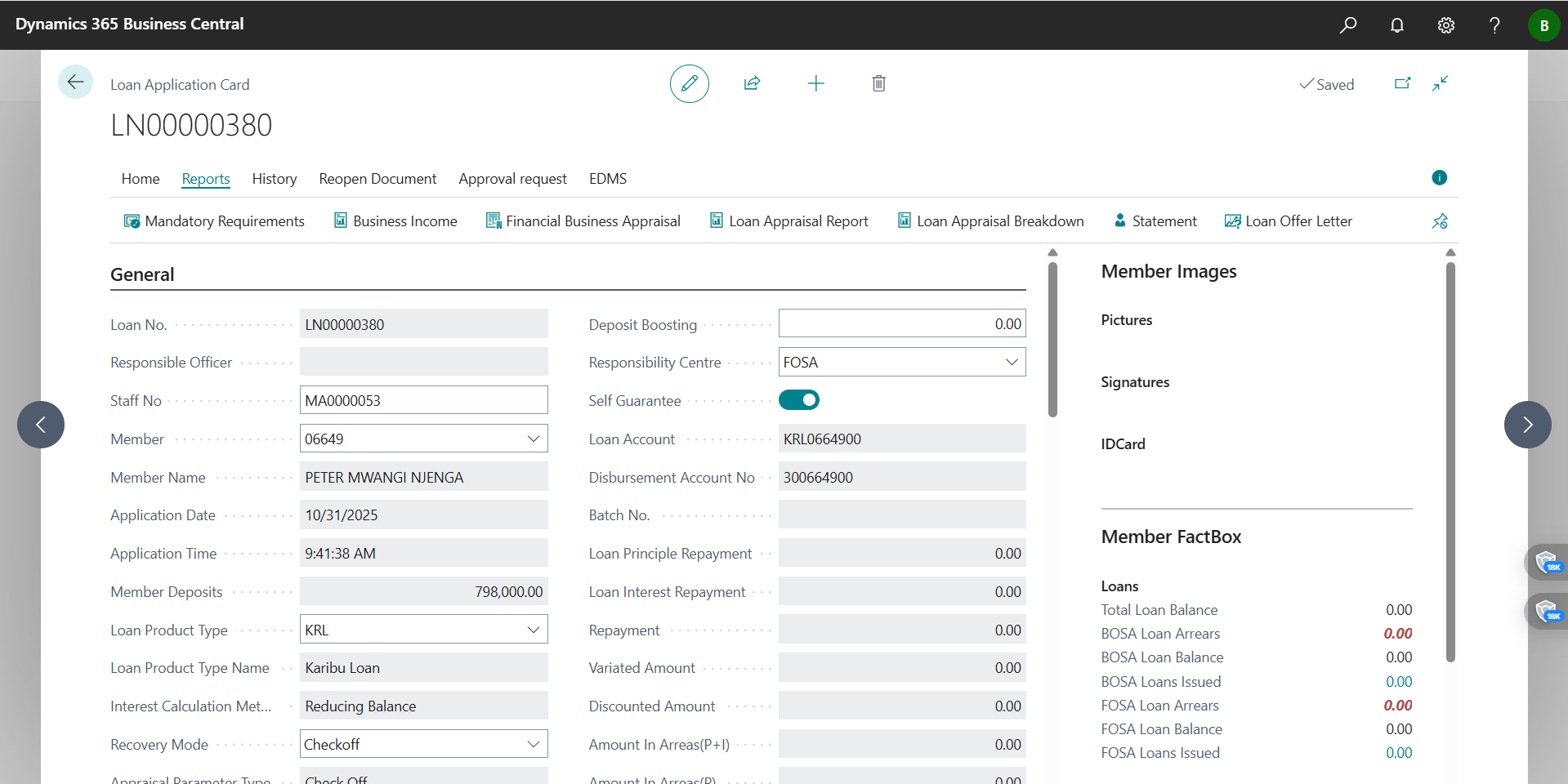

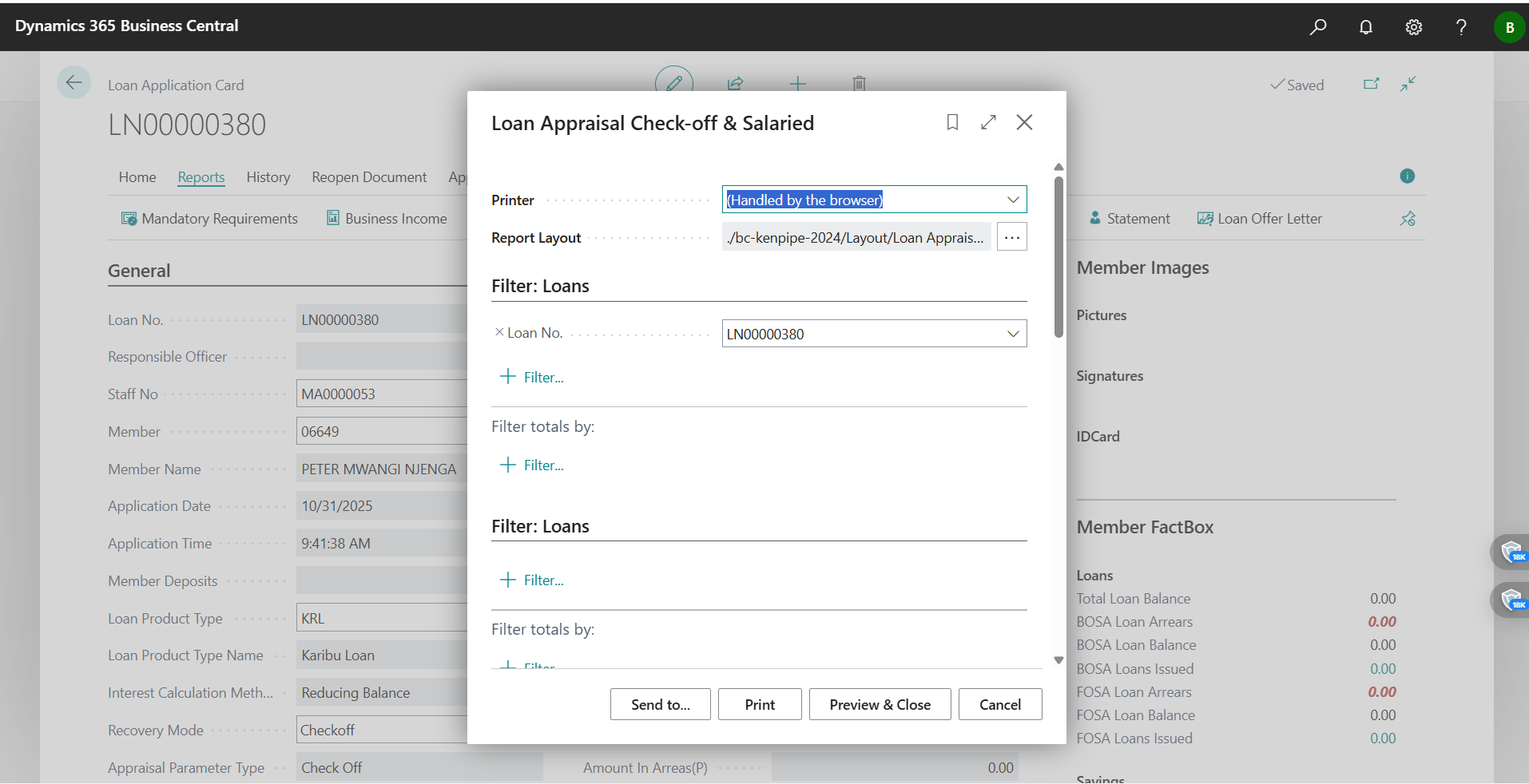

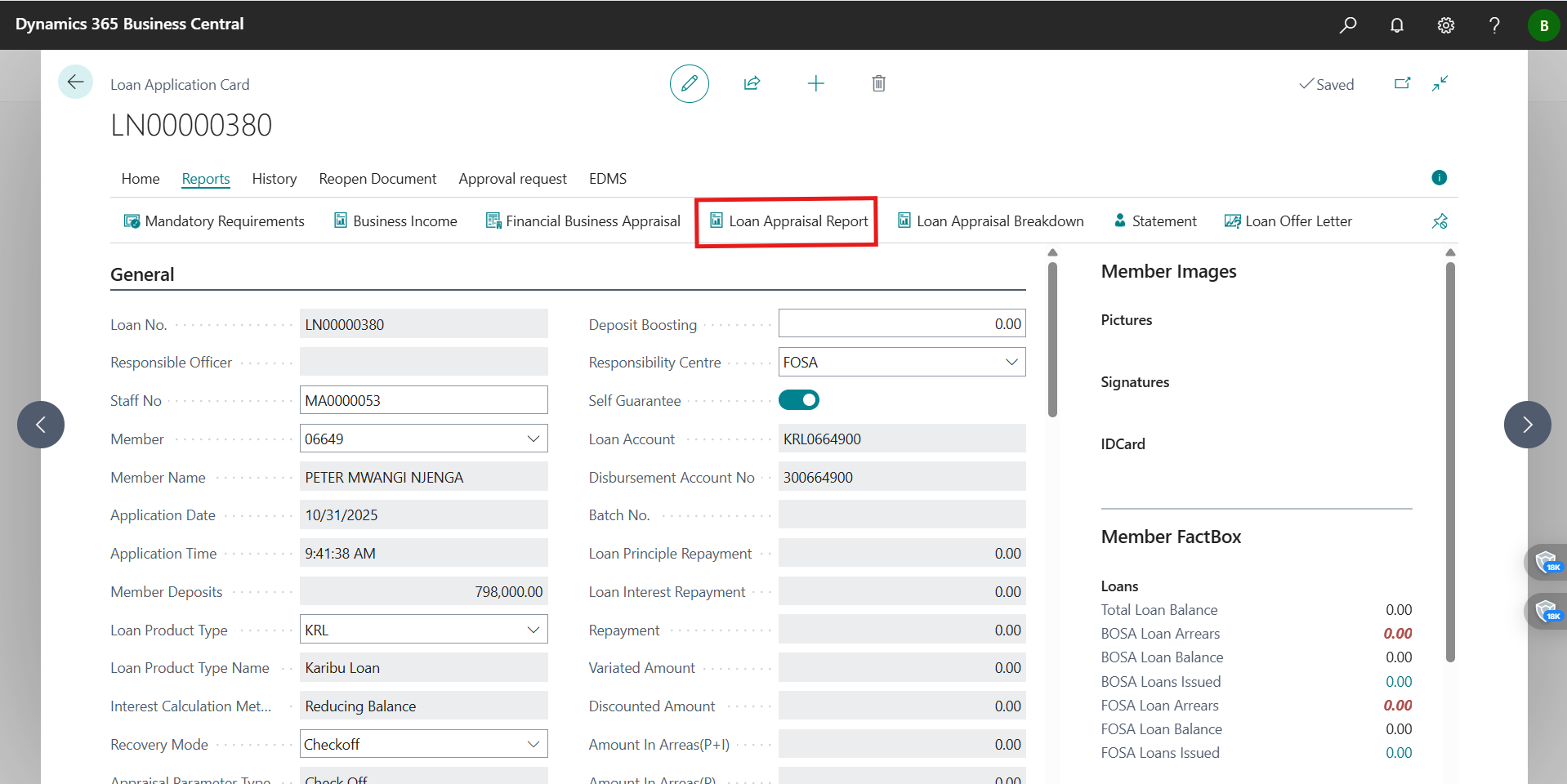

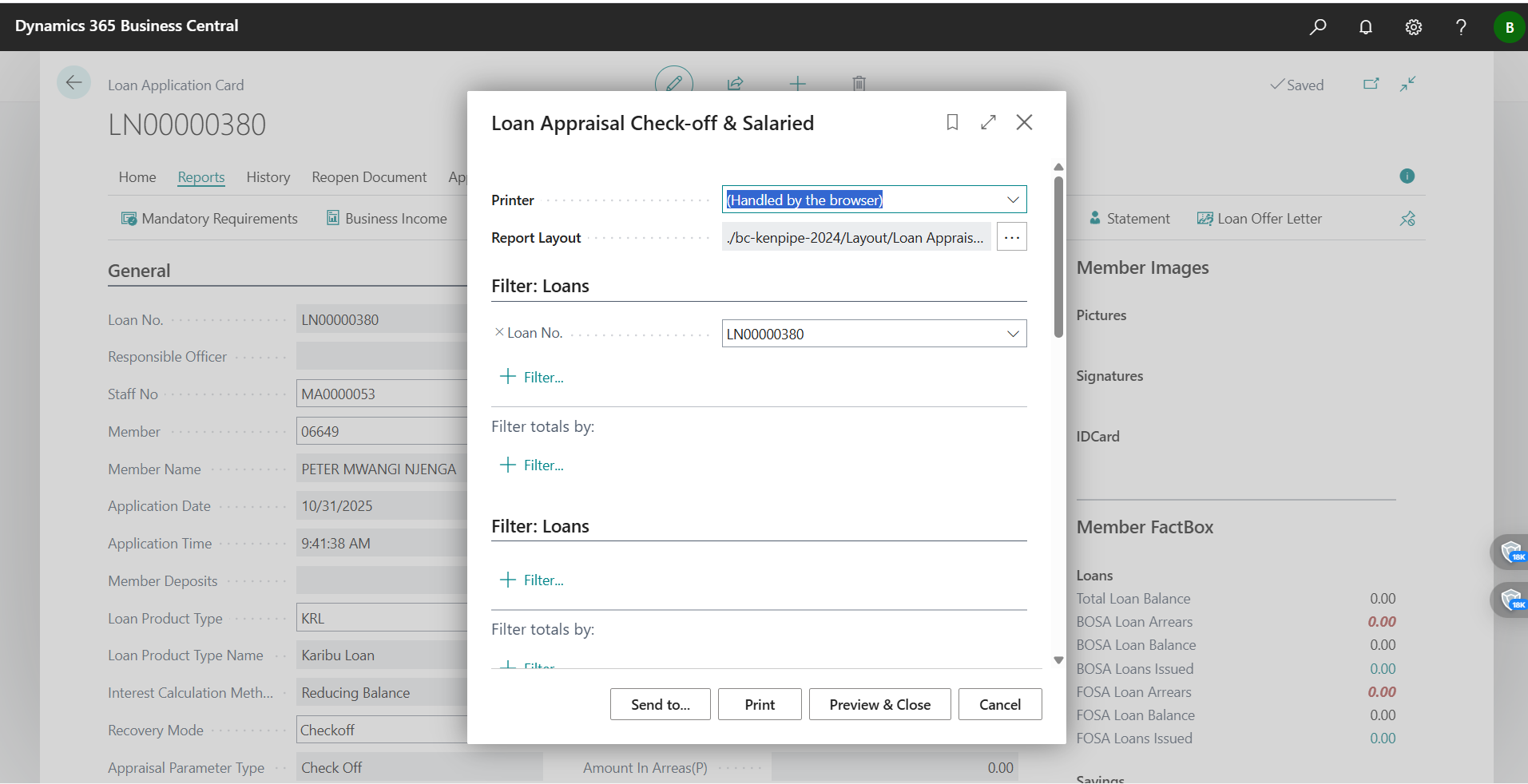

Step 5 — Generate and attach the Appraisal Report

- Use Appraisal > Generate Appraisal Report to compile the formal memo for approval.

- Verify it includes member profile, incomes/obligations, collateral/guarantors, eligibility KPIs, schedule summary, and any conditions; then I attach the PDF to the application.

- Visuals:

- Action:

- Preview:

- Action:

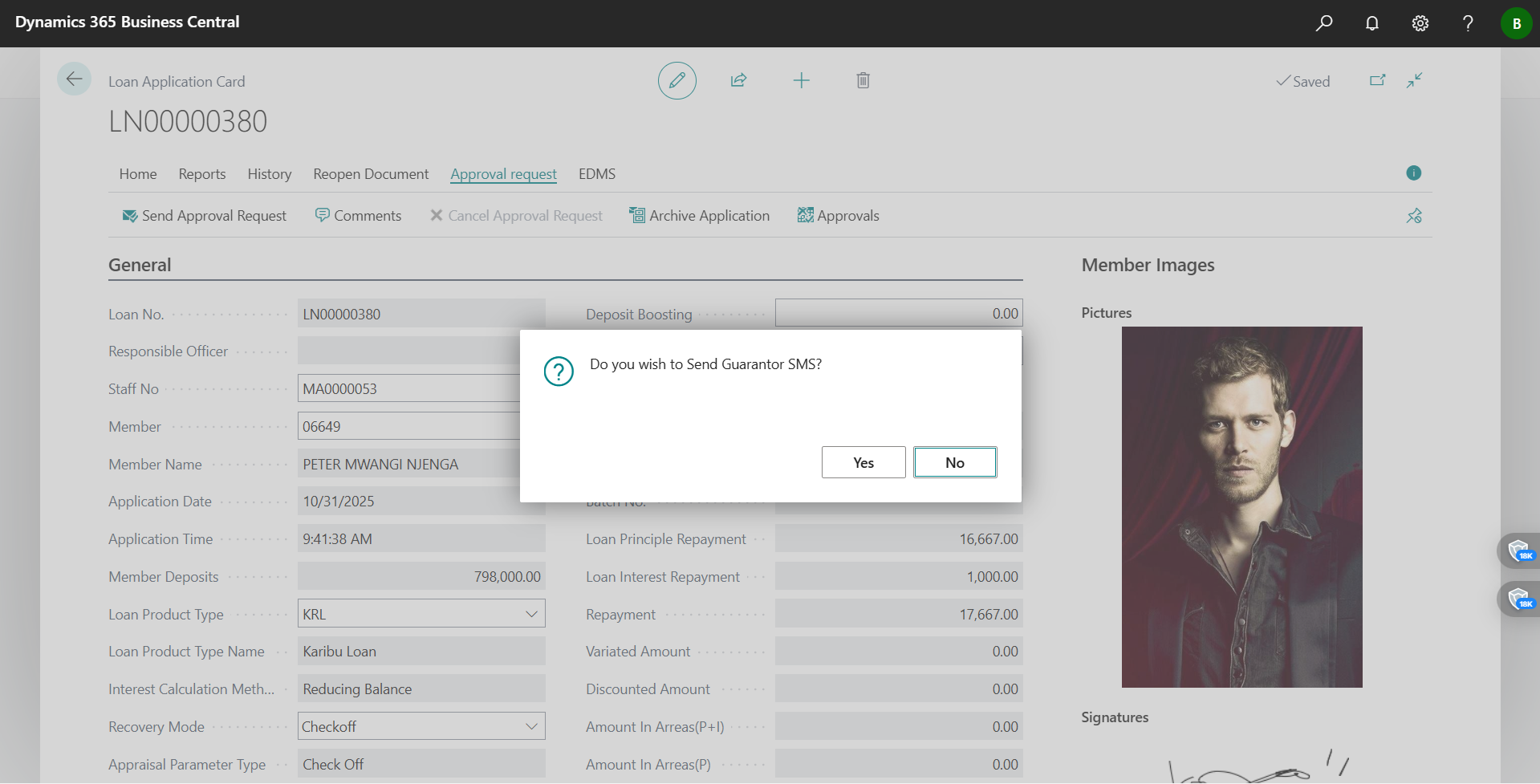

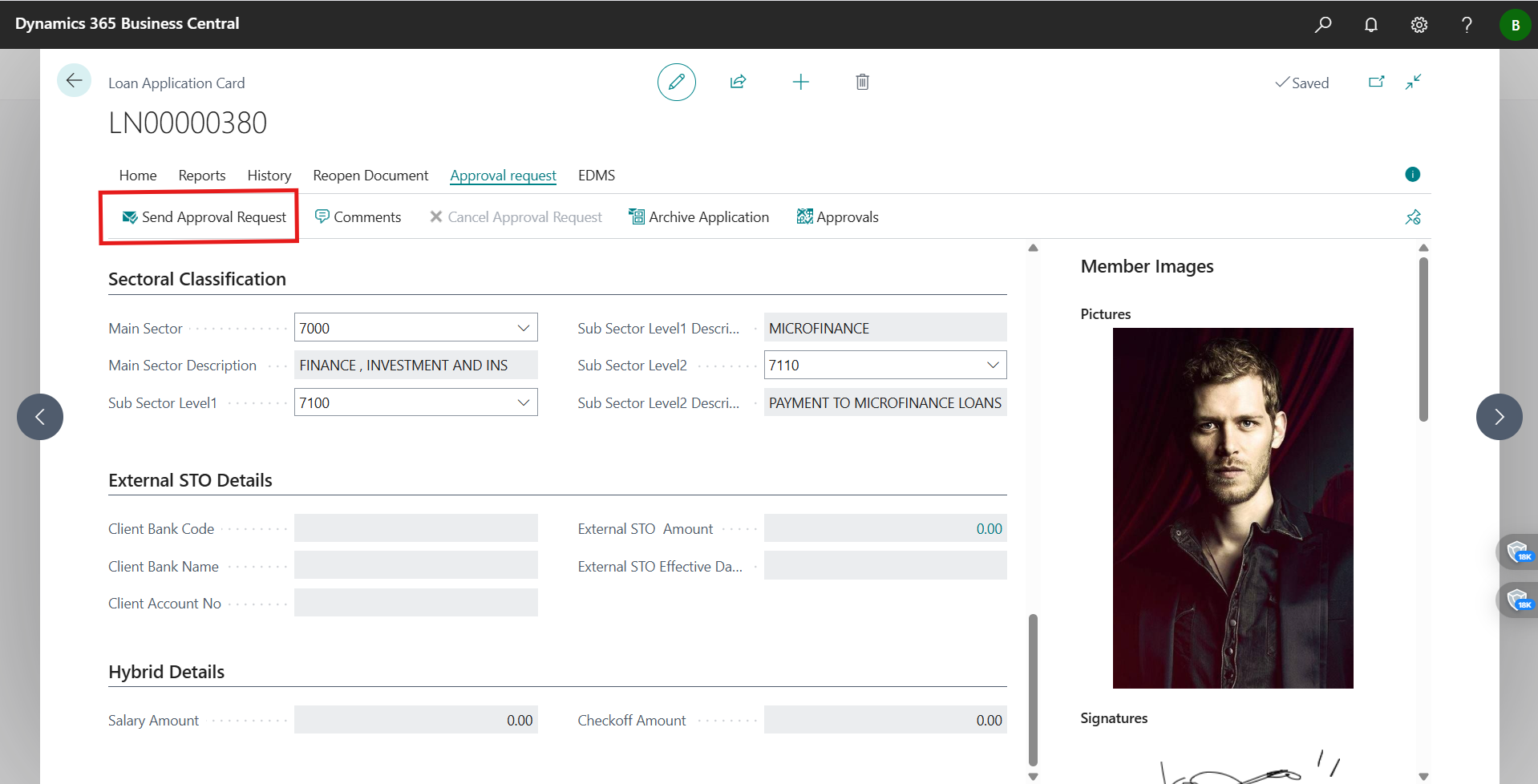

Step 6 — Send the appraised loan for approval

- From the application, click Send for Approval and add a short message: recommended amount/term, any exceptions, and key conditions (e.g., extra guarantor, share top‑up).

- Visual:

- Result: Approval Entries are created and the document locks while it’s pending.

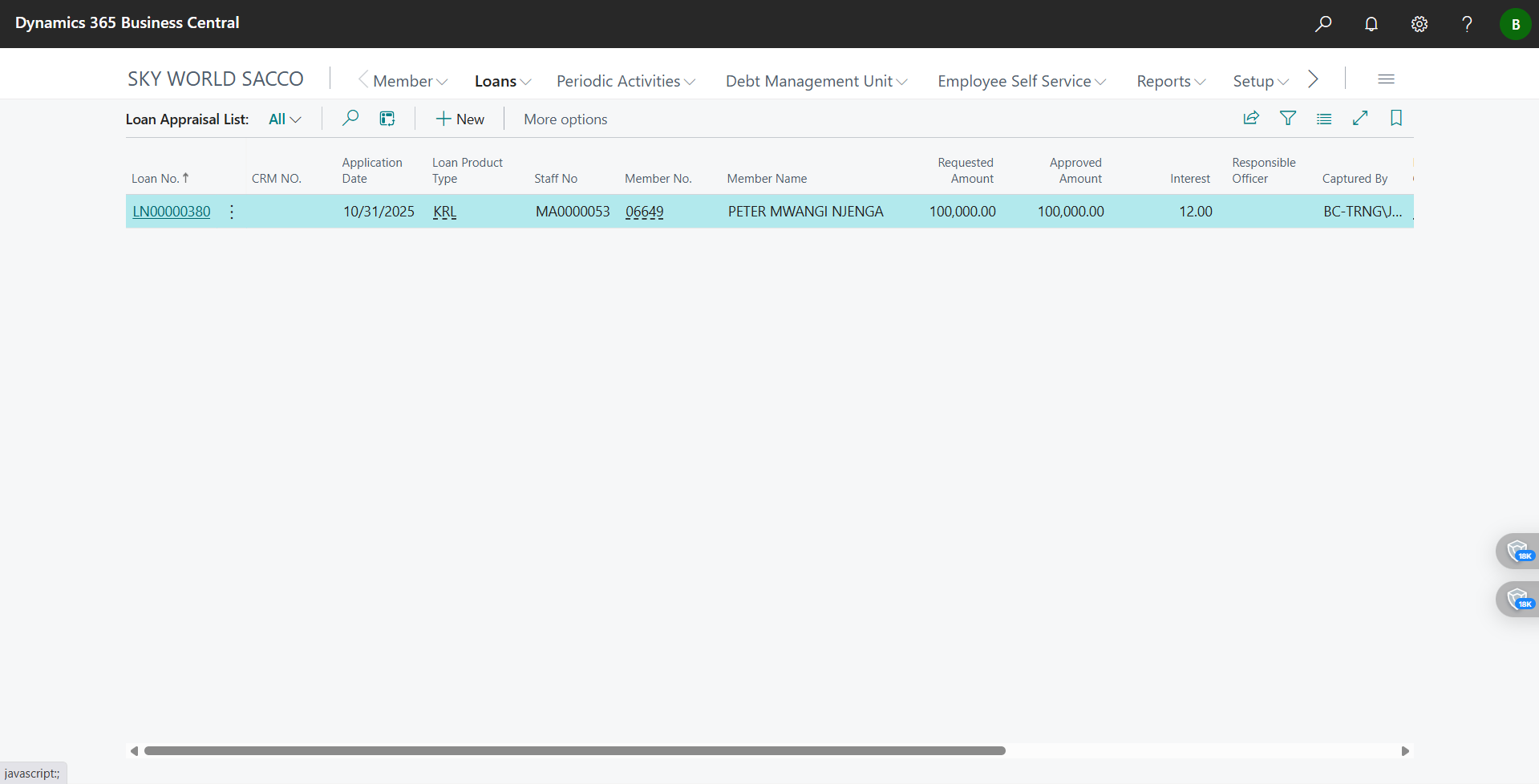

Step 7 — How the approver acts on the request

- The approver opens Approvals > Requests to Approve, opens the loan, and reviews my Header, Appraisal/Financials, Collateral/Guarantors, Schedule, Attachments, and the Appraisal Report.

- Visual:

- Actions they can take (as shown): Approve, Reject (with a comment), Delegate, or Request Changes. I always read their comments for the audit trail and re‑submit if asked.

What each screenshot proves in my flow

- appraisal button.png — Where I access the Appraisal menu on the application card.

- Loan Appraisal Breakdown.png — The live eligibility KPIs I reviewed (share multiple, DTI, recommended amount/term).

- loan eligibility breakdown.pdf — The detailed numbers I relied on for the memo.

- Generate Payment Schedule.png — The exact parameter dialog I used to validate affordability.

- generate appraisal report.png & preview Appraisal Report.png — The report action and the preview I checked before attaching.

- send loan for approval.png — The action I used to trigger the workflow.

- Approval actions.png — The approver’s decision buttons I expect them to use.

- Screenshot 2025-10-31 *.png — The application pages/tabs I edited and double‑checked during appraisal.

The data I make sure to capture before approval

- Member & Product: Member No./Name; Product Code/Name

- Amount & Tenor: Requested vs. Recommended Amount; Requested vs. Recommended Term

- Income & Obligations: Gross/Net monthly income; other recurring income; existing installments; deductions/expenses

- Eligibility KPIs: Share‑multiple cap; DTI; net pay/allowable deduction; exceptions and rationale

- Collateral/Guarantors: Values and coverage %; guarantor exposure/limits

- Schedule summary: Frequency; first installment date; total interest/repayment

- Attachments: Appraisal Report PDF; appraisal form; eligibility breakdown PDF; KYC evidence

How I keep control and a clean audit trail

- I rely on maker‑checker via approvals so my document locks while pending.

- I put concise, decision‑ready comments in the approval message and attach the PDFs.

- I keep all adjustments (like conditions or exceptions) written in both the report and approval comments.

If I hit a snag (what I do)

- Appraisal actions not visible → I confirm I’m on a Loan Application card, have permission, and the product is Released.

- Eligibility Breakdown empty → I re‑enter missing income/obligations/product data and run it again.

- Can’t generate schedule → I fill principal, rate, term, frequency, and first installment date; then retry.

- Appraisal Report won’t open → I check that the report is published and allow pop‑ups.

- Can’t send for approval → I confirm Approver User Setup, workflow activation, and approver limits.

- Approver can’t act → I check Approval Entries for delegation or substitutes and nudge the current assignee.

Appendix — The exact images and documents I used

- loan eligibility breakdown.pdf

- Context screenshots I referenced: